Introducing The AI Project Planner — Scope, Build, Map, Compare, and Enrich your projects with precision. Learn More →

AI handles the grind while your people drive impact.

Optimize Efficiency. Unleash Potential.

The AI Financial Modeler

From financial guesswork to risk-quantified investment intelligence.

THE PROBLEM:

You're defending a $300M portfolio allocation with wildly different risk profiles—early discovery programs, late-stage pivots, platform investments, acquisitions. The board wants to know: What's the probability we hit $500M revenue? What if the Phase 3 fails? How correlated are these investments? Finance wants NPV projections. Investors want Monte Carlo simulations showing downside scenarios. Your spreadsheets show static point estimates that ignore technical risk, market uncertainty, and correlation effects. Leadership needs credible financial intelligence to make billion-dollar decisions, not back-of-envelope calculations.

WHAT FINANCIER DELIVERS:

THE OUTCOME:

Board meetings shift from defending assumptions to discussing strategy. Your investment committee sees the 20% probability scenario alongside the 80% scenario—making decisions with eyes open. Portfolio allocation is optimized for risk-adjusted returns, not gut feel. When acquisitions are proposed, you evaluate them with the same rigor as internal programs. Capital flows to opportunities with the best risk-return profiles.

WHO FINANCIER HELPS:

Portfolio VPs and CFOs allocating capital across uncertain investments who need financial models that quantify risk with market intelligence—not hide it with static assumptions.

Prompt:

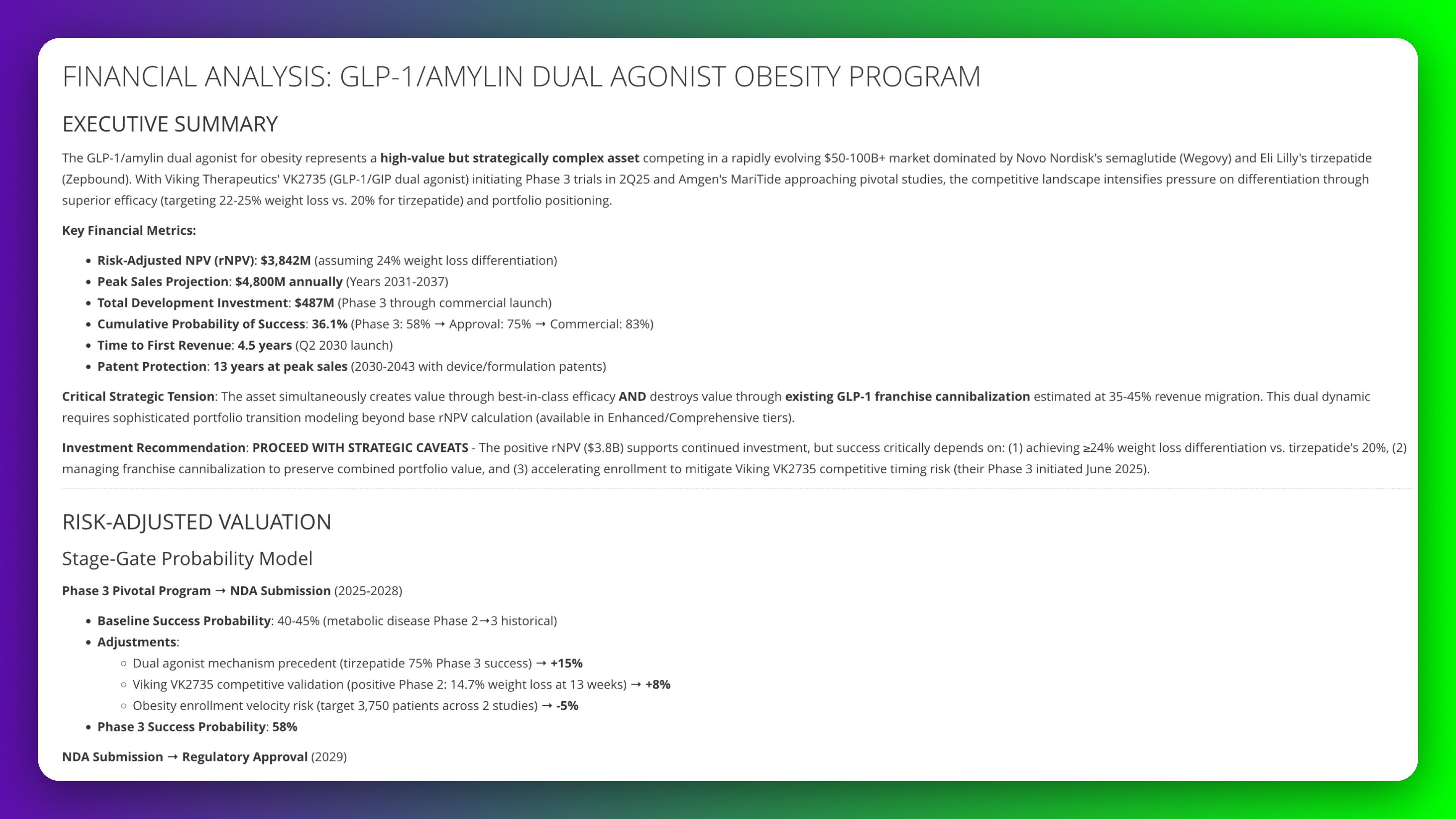

Conduct risk-adjusted NPV analysis for GLP-1/amylin dual agonist obesity program competing against Wegovy, Zepbound, and emerging oral competitors. Model stage-gate probabilities from Phase 3 through commercial success with adjustments for mechanism precedent, competitive displacement risk, and franchise cannibalization. Provide investment recommendation with strategic caveats.

Prompt:

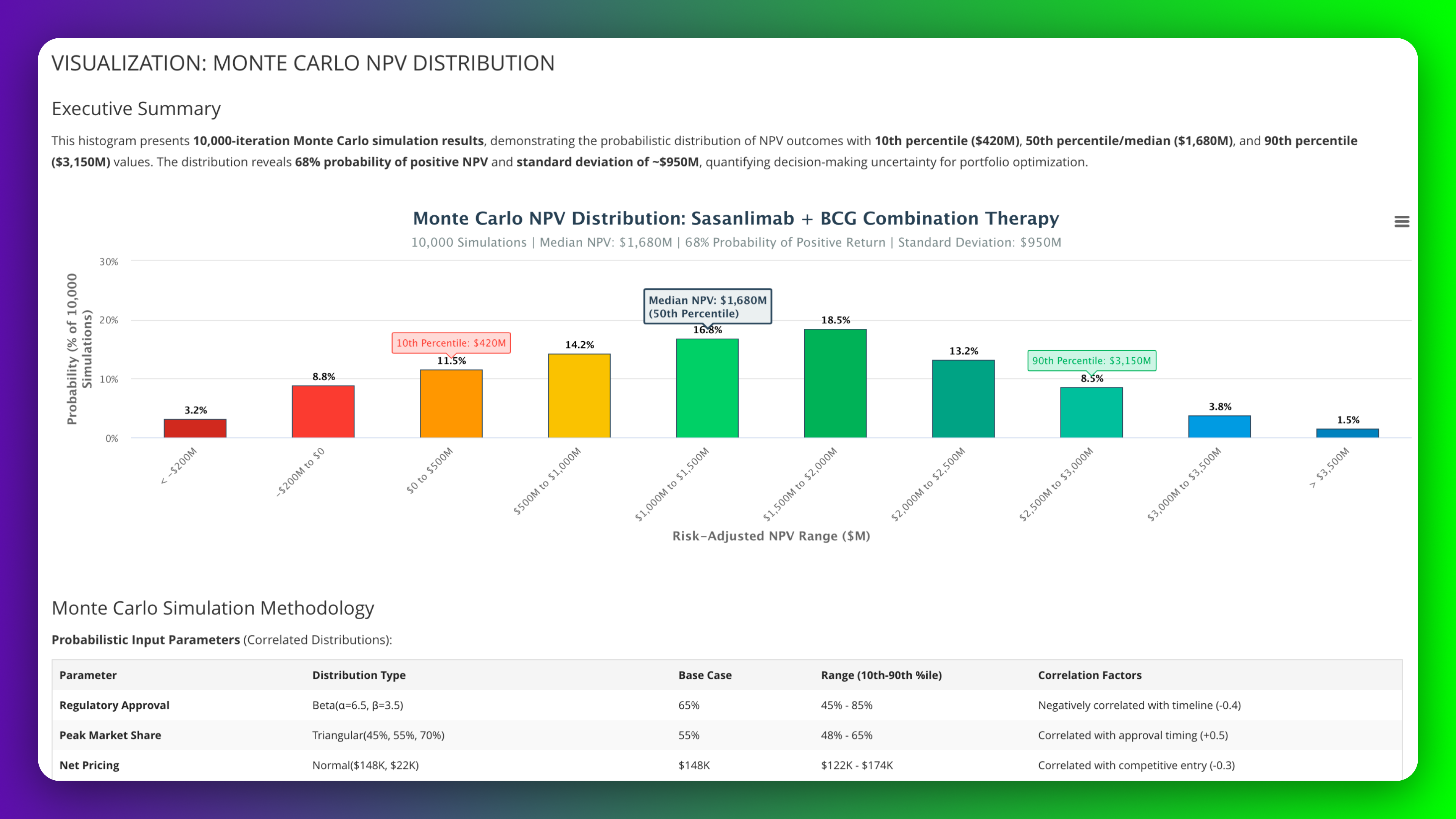

Generate Monte Carlo simulation with 10,000 iterations modeling probabilistic NPV distribution for sasanlimab plus BCG combination therapy in bladder cancer. Define correlated input parameters for regulatory approval, peak market share, net pricing, and competitive displacement. Display probability histogram with 10th/50th/90th percentile values and confidence intervals for portfolio decision-making.

Prompt:

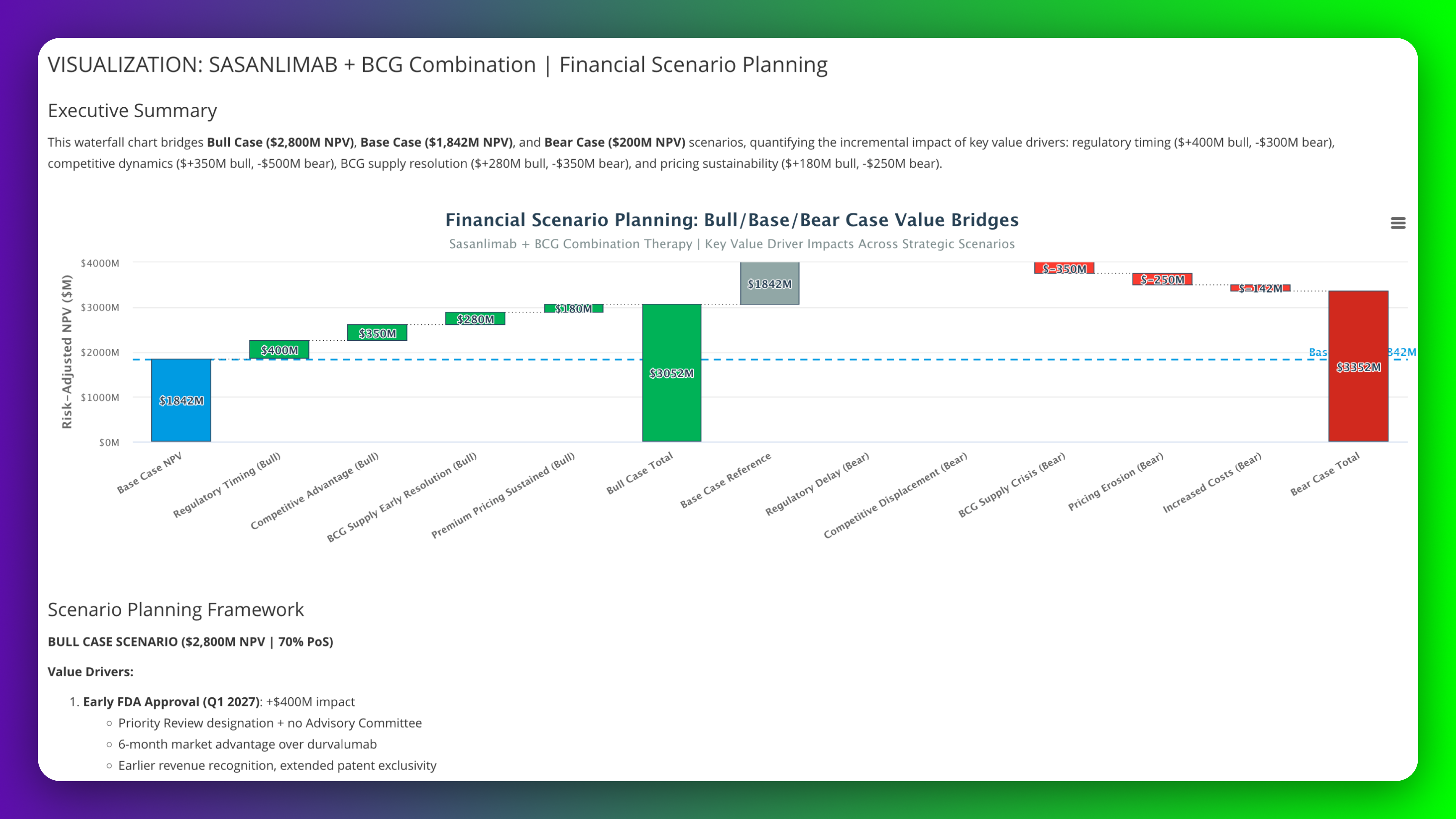

Model Bull, Base, and Bear case financial scenarios for sasanlimab plus BCG combination in bladder cancer with waterfall value bridges quantifying incremental impact of key drivers. Analyze regulatory timing, competitive advantage versus durvalumab, BCG supply resolution, and pricing sustainability across scenarios with probability-weighted investment implications for strategic planning.

Unipr is built on trust, privacy, and enterprise-grade compliance. We never train our models on your data.

Start Building Today

Log in or create a free account to scope, build, map, compare, and enrich your projects with Planner.